In our view the ‘Quick Fix’ is neither quick nor a fix. That said, some of the unintended consequences of implementing the MiFID II requirements, e.g. ‘voice digitisation’, have in fact been much more beneficial to the industry than the intended outcomes the regulators envisaged. Below we explain why and step you through the main changes.

In February/March the EC produced a series of proposed amendments to the MiFID II directive that we referenced in a piece earlier in the year. Then in late July the Commission made a further announcement proposing measures designed to alleviate some of the pressures created by COVID as a first step in the MIFID II Review.

Some of the areas affected by the changes worth calling out:

- Best Execution (RTS 27) and possibly top 5 venue reporting (RTS 28)

- Unbundling of fixed income SME research

- Systematic Internaliser (SI) regime and pre trade transparency

Below we explore the proposals in more detail and provide some commentary:

1. Best Execution (RTS 27) and top 5 venue reporting (RTS 28)

Best execution reporting (RTS 27) and top 5 venue reporting (RTS 28) were a hotly debated topic when MiFID II was being implemented all those years ago however now we’re seeing real changes being tabled to these requirements. The amendments introduce a delay to the requirements for venues and SIs, to provide best execution reports as detailed in RTS27. This delay is for 2 tiers from entry into force of this amending directive, so probably moves this requirement out to 2023

Why the proposed changes?

- Best execution reports are believed to not be widely read

- Concerns on the accuracy of reported data for non-bond products, stemming from the bad ISIN3 schema – maybe this should be the focus.

Although not contained in the ‘Quick Fix’, many are also calling for RTS 28 to be shelved since the reports are rarely read and even to those who do, the reports don’t necessarily give real insight into business concentration.

So what do we think?

A lot of trouble at the time...

Transparency and pre- & post-trade reporting were behind a large share of the spend and efforts in 2017/2018 but the most far-reaching requirements were under the ‘best execution’ (RTS27) and ‘quality of execution’ (RTS28) labels. Some of the quarterly reports require participants to capture precise timestamps (1 second granularity) at every step of the negotiation process and for the vast majority of products (from gilts to very complex structures). This is trivial for electronic flows but much more problematic for voice negotiations.

Manually capturing these timestamps is time-consuming, very inefficient and isn’t really an option when other requirements (such as pre-trade transparency) may apply. This is why many participants built platforms to digitise these voice workflows, in effect enabling their sales force to turn voice inquiries into electronic flows. These were initially met with reservations as the steps to digitise these flows were perceived as likely to impact the speed of the inquiry/quoting process.

...but worth it in the end

Once people started getting used to the new tools and processes, these reservations were gradually replaced by a realisation that digitising these flows had major benefits. Dealers were providing clients with faster and more precise quoting, execution and booking, while keeping their risk accurate with real-time updates. These benefits soon outstripped what was initially perceived as the inconvenience of getting used to new processes.

...though not for the reasons intended

While this epiphany was taking place, it was also becoming clear that RTS27 & 28 reports, which should conceptually have been great sources of information for all market participants, were not being used.

One reason is that the accuracy of the reports for derivatives was questionable: the underlying data was captured at ISIN level and the way these ISINs were derived faced some challenges. For instance, effective dates were not initially required to generate an ISIN, so in effect an IRS4 starting in 5y with a 5y tenor would have the same ISIN as a spot-starting IRS with a 10y tenor. Putting aside data quality, most participants also had better ways to get information found in RTS27 & 28 reports, for instance from broker reviews.

For these reasons, the ‘Quick Fix’ recommendation to suspend (potentially indefinitely) the production of these reports for derivatives seems appropriate. We are however in a situation where the industry has already heavily invested in digitisation to produce these reports and we believe it is very unlikely this suspension will have any impact on current practices.

Whilst voice digitisation was initially imposed upon people to meet regulatory requirements, it has since become so strategic that these tools and processes are bound to continue expanding with or without these requirements. Some could see this as a large-scale wasted investment, we believe it had the effect of accelerating a voice digitisation agenda that is benefiting the industry beyond the scope of MiFID II.

We are of the opinion that the aforementioned suspension could potentially slow down the digitisation of more complex products – but for most dealers, it is very likely this will still continue to happen at pace, with or without these regulatory requirements.

NatWest Markets took a big step in this space last year by starting to offer a ‘digital voice’ channel directly to clients (the ‘Scout’ chatbot), leveraging the internal voice digitisation platform that was initially built to meet MiFID II requirements. This hybrid of voice and electronic enables our clients to stream prices into chats, publish our axes into chats on-demand, execute and automatically book trades directly from the chat and seamlessly capture and report timestamps.

2. Research unbundling

The regulation currently details rules stipulating that investment firms must charge certain clients (e.g. fund managers) for research, and must do so separately from execution services. This was a hotly debated part of MiFID II, specifically access to key material the industry ‘needs’. The amendment removes these stipulations, specifically:

"By way of derogation from paragraphs 1 to 8, an investment firm can choose not to comply with the requirements set down in those paragraphs in either of the following cases:

- the research is exclusively provided on issuers which did not exceed a market capitalisation of EUR 1 billion during a period of 12 months preceding the provision of the research;

- the research is exclusively provided in relation to fixed income instruments"

Like I've commented on other regulatory changes, removing some parts of the requirements can lead to operational complexity and one wonders whether the best result would be to exclude FX from this ‘fix’ or simply leave as it is, noting the efforts to get us to this point.

3. Systematic Internaliser regime (SI)?

Outside of the ‘quick fix’, ESMA5 published a report in July that reviews the pre-trade transparency obligations applicable to systematic internalisers in non-equity instruments. A few highlights:

- ESMA found that the definition of firm quotes underpinning the publication obligation under article 18(1) MIFIR6 was well understood and needed no further clarification;

- Similarly no further defining of what constituted exceptional market conditions (article 18(3)) under which an SI could pull a firm quote for other clients in a liquid instrument were considered necessary.

- ESMA concluded that there was no purpose served in making SIs hold prices in liquid instruments open for other clients other than the requesting client.

- Finally, ESMA saw no merit in requiring provision of pricing in illiquid instruments to requesting clients where previously provided under article 18.2.

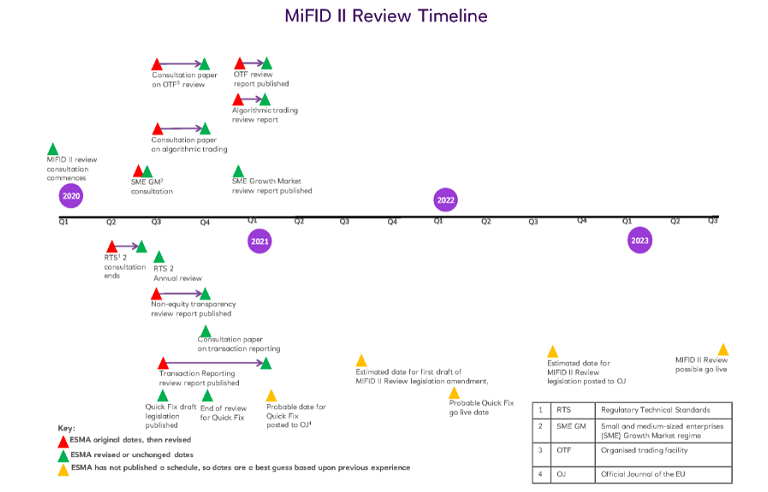

MiFID II review, then consultation delays and now the Quick Fix...

so what's happening when?