Regulation

LIBOR fallbacks….and the winner is…..5 year median

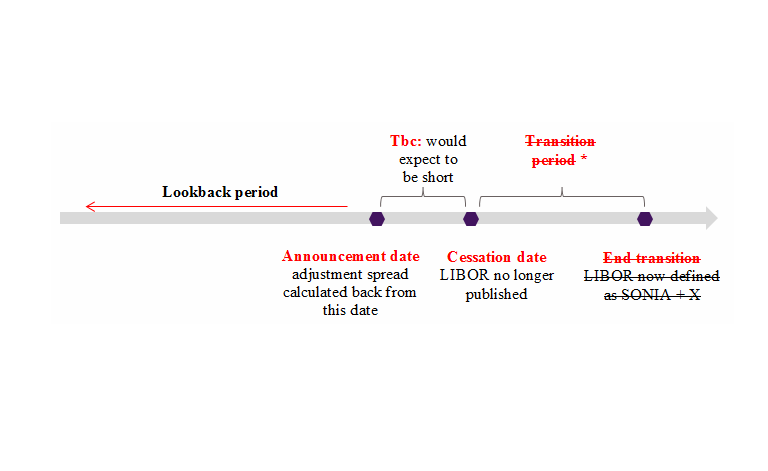

In what seems like an endless stream of consultations, the International Swaps and Derivatives Association (ISDA) finally give us clarity on the fallback mechanics for derivatives at least, even though there's confusion as to what triggers this.

18 Nov 2019

We're impressed how quickly the results on fallback rate mechanics have been announced since our recent note. The pace has certainly picked up and it needed to.