Regulation

ISDA LIBOR fallback protocol - better late than never?

So it’s finally here!

09 Oct 2020

. 6 min read

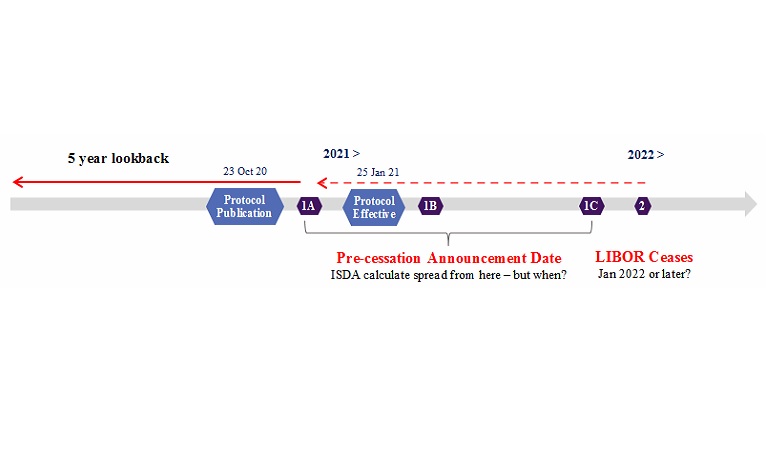

The ISDA[1] Fallback Protocol first anticipated back in the heady pre-COVID days in September last year will be published on 23 October 2020 and become effective on 25 January 2021. A critical milestone in LIBOR[2] transition.