Regulation

Down the road... 2022 regulatory look ahead

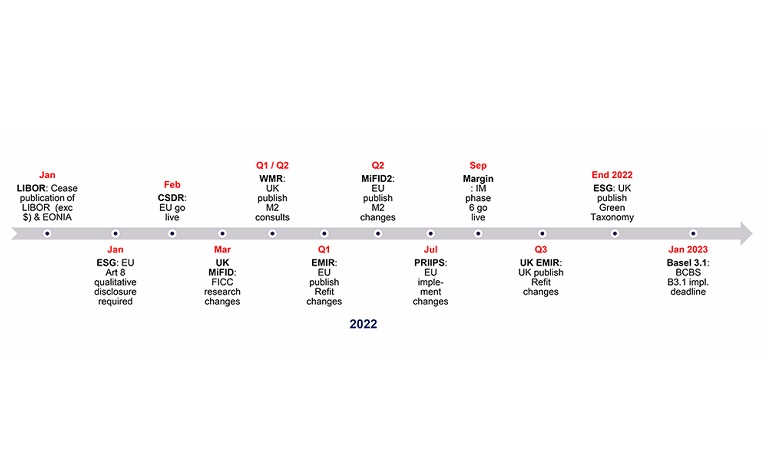

In what is becoming a new year’s tradition we take a look below at what we think the main regulatory themes will be in the year ahead.

11 Jan 2022

Looking back on 2021, clearly LIBOR played a big part, ending not so much with a bang but a whimper. Year-end activities seem to have gone smoothly and we’re getting used to the new normal. ESG also dominated the agenda, and we expect to see this gain ever greater focus in the year ahead.