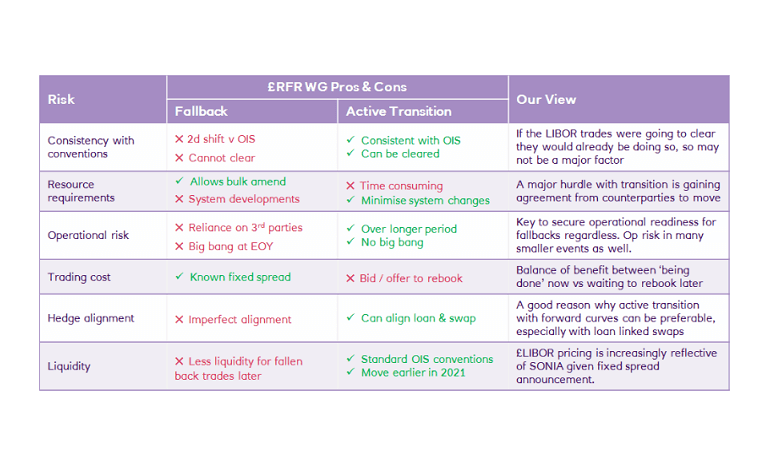

Fair to say the official sector is firmly in the “act now” camp. Numerous statements have been made recently (see the Roadmap and the Dear CEO letter for example) encouraging the market to actively transition from LIBOR[2] to RFR[3] now. Risks of leaving it until later or depending on fallbacks are listed in these recent papers – loss of liquidity in LIBOR, operational risk and hedge misalignment etc.

However there has also been a huge push to get everyone to sign-up to the ISDA[4] Fallback Protocol. And it has been very successful – 13,862 legal entities signed-up at the last count covering the vast majority of open notional in LIBOR-linked linear derivatives in the market. What is the point of all this adhering if actually everyone needs to actively transition? We are seeing counterparties that consider waiting for fallbacks to kick-in to be a perfectly valid transition strategy.

So what’s the answer – jump now or hang on?

Spoiler alert – there is no single answer, it will depend upon your particular circumstances, hedging dependencies, risk appetite, operational readiness and no doubt a host of other factors. Though one thing we can say is that doing nothing is not a good option...if you have no fallbacks in place and have not actively transitioned, then you will face challenges come cessation.

Below we try to set-out some of the main paths available, and our take on the pros & cons of various options.

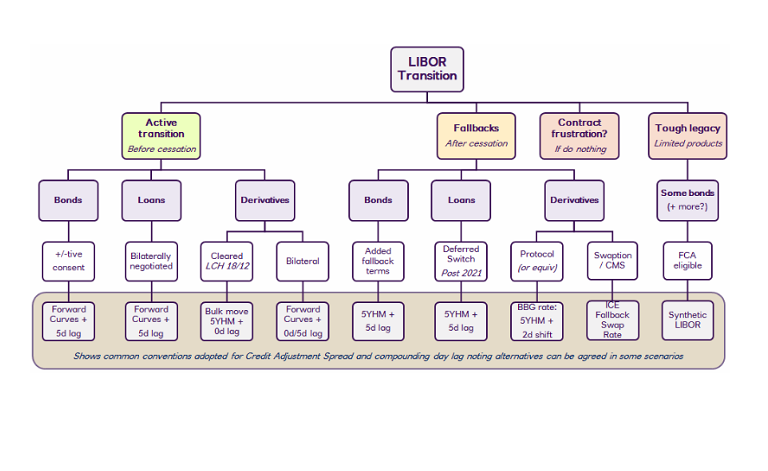

What are my options?

First thing to say is not all fallbacks are created equal. Or more accurately, there are plenty of transactions where fallbacks are hard or impossible to implement, and realistically active transition is the only option. Many cash products, across both bonds and loans, fall into this category – they do not have robust fallbacks built-in today, and rather than attempt to negotiate them now it is easier just to negotiate the transition to RFR.

It’s a different story for derivatives, where there is a very clear and robust fallback solution available that has been widely adopted in the market. That’s not quite the whole story though, as where those derivatives hedge cash products there may be a need to retain alignment, and that might be best effected by active transition of both loan & swap together.

And Although I say that the ISDA protocol has been ‘widely adopted’, really I mean it has been widely adopted across financial institutions where most of the open swap notional resides, however it is not nearly so widely adopted amongst corporates. The exposure there may not be so material from a market perspective, however the number of legal entities affected could still be high.

Then there are some non-linear derivatives where either the ISDA Fallback Protocol does not apply (e.g. Swaptions and CMS[5] that reference the LIBOR ICE Swap Rate when cash settled) or it does apply but changes the economics or behaviour of the trade (e.g. some Caps & Floors). Active transition rather than reliance on fallbacks might be a better option there.

Finally, there is something of a hybrid emerging as an increasingly popular option in the loan market. Often referred to as “deferred switch”, the borrower and lender(s) negotiate the amendment of the terms of the loan to RFR + a credit adjustment spread now, but it does not come into effect until the first reset date after cessation. So, it is a quasi-fallback solution even though referred to as a ‘switch’ and could equally well be considered as ‘active transition’. Distinction is just the timing – is the deferred switch date before or after cessation.

In the below diagram we set out in simple terms the main paths that can be followed, across active transition & fallbacks, and across the main asset classes. At the bottom we show common outcomes for the conventions used when moving to RFR (based on Sterling market, appreciating USD and other markets may vary). Disclaimer – we are not trying to set out all the options and outcomes here, just give a flavour for the alternatives.