Markets

UK Budget 2021 debrief: reasons treasurers can feel positive about the UK outlook… for now

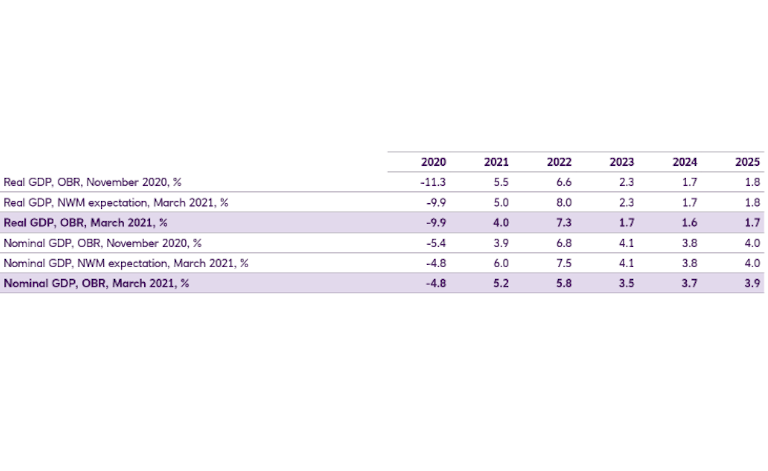

A more modest recovery: the UK government revised its economic outlook downward, albeit marginally, from 2021 onward.

05 Mar 2021

. 5 min read

“Pay now, tax later” will help support corporate sectors near-term: a larger-than-expected fiscal stimulus – a final push, as it were – will support businesses across the economy.