On this page:

Overlay

De-dollarisation, geopolitics and trade

The Year Ahead 2026

Monetary policy in 2026: is it terminal for rates?

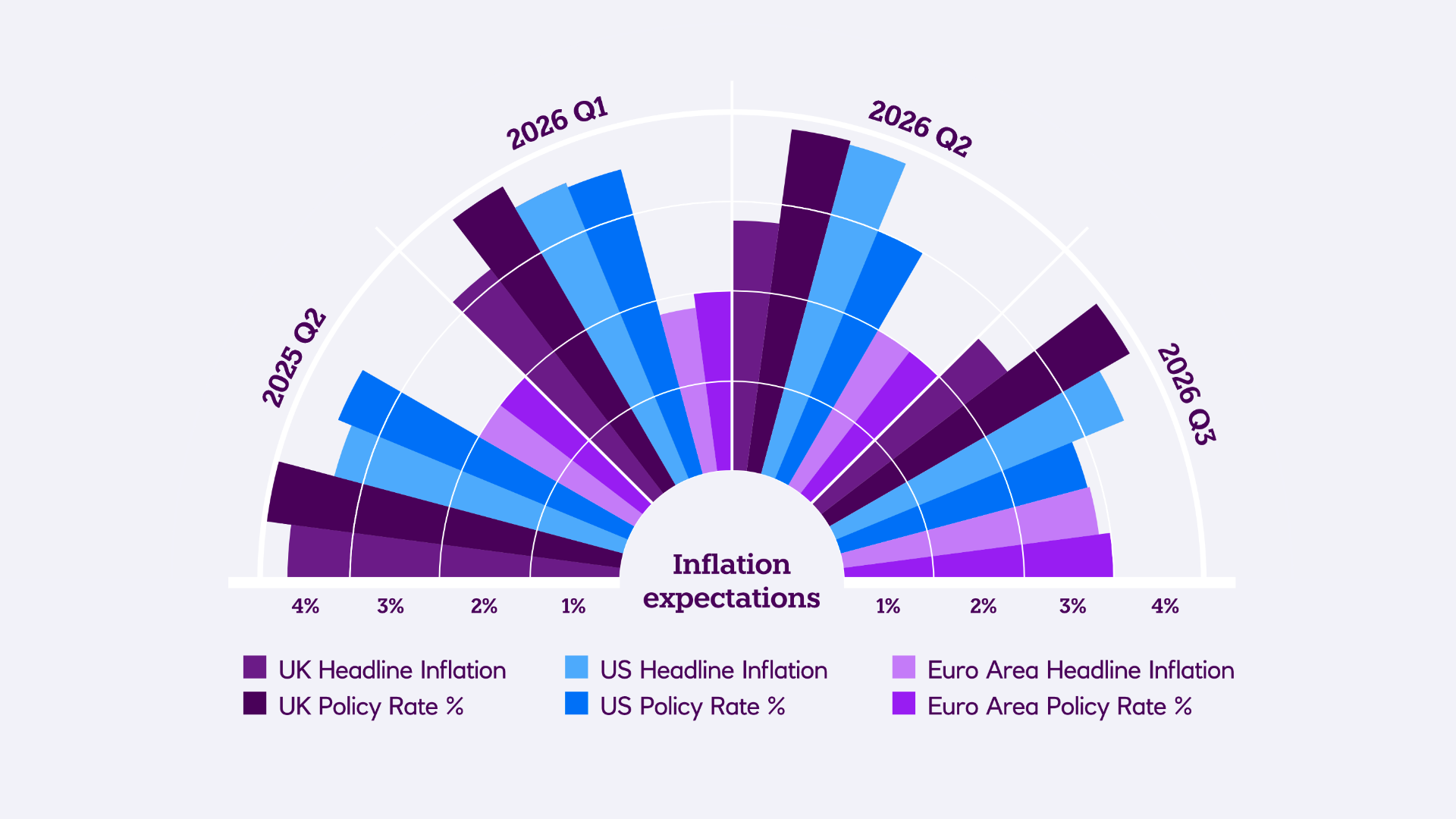

The worst of inflation is over, for now, but what next for policymakers in major economies?

At a glance:

US inflation is an open question, beset by issues around labour and tariff influences.

Stubborn price levels in the UK suggest no hasty cut to 3% rates.

The eurozone has reached target inflation and rates look terminal.

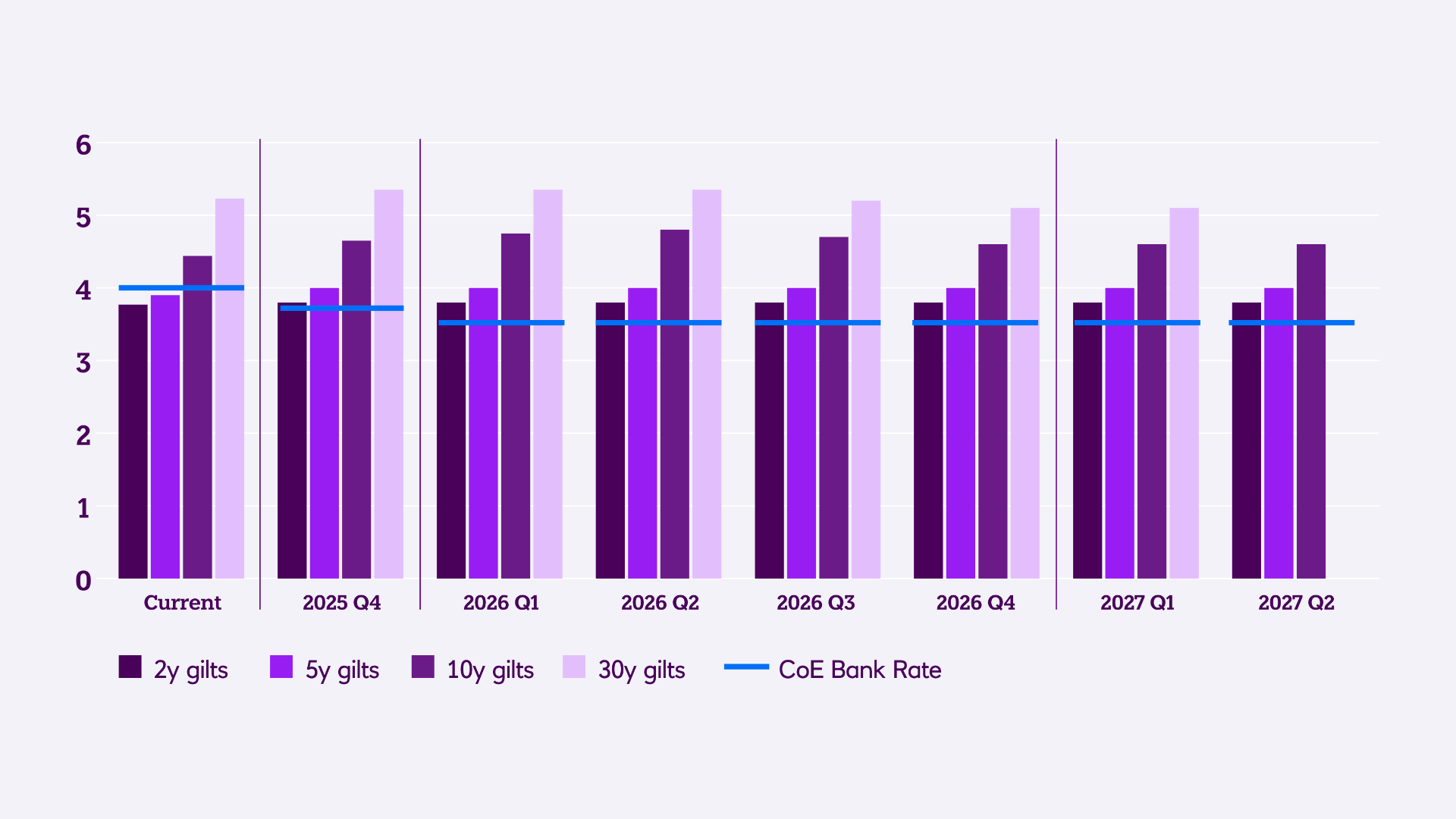

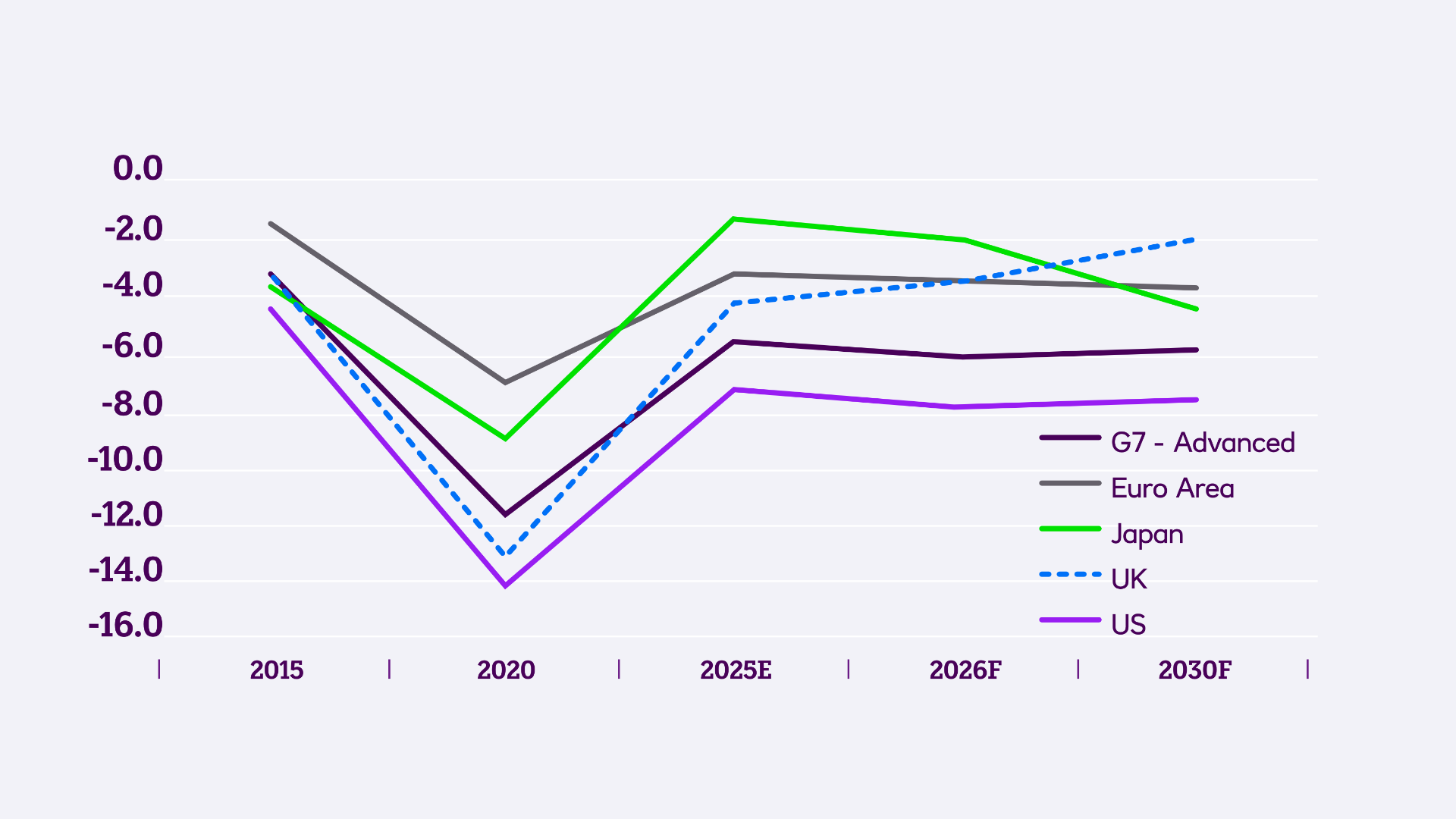

Fiscal frailties: is national debt a concern for markets in 2026?

Major economies face sluggish output growth – a problem for the sustainability of government borrowing (and bond markets).

At a glance:

High debt levels, including debt servicing costs, persist into 2026.

The yield curve is likely to steepen at the long end as a result of fiscal debts.

Structural shifts in markets present a question for the EU.

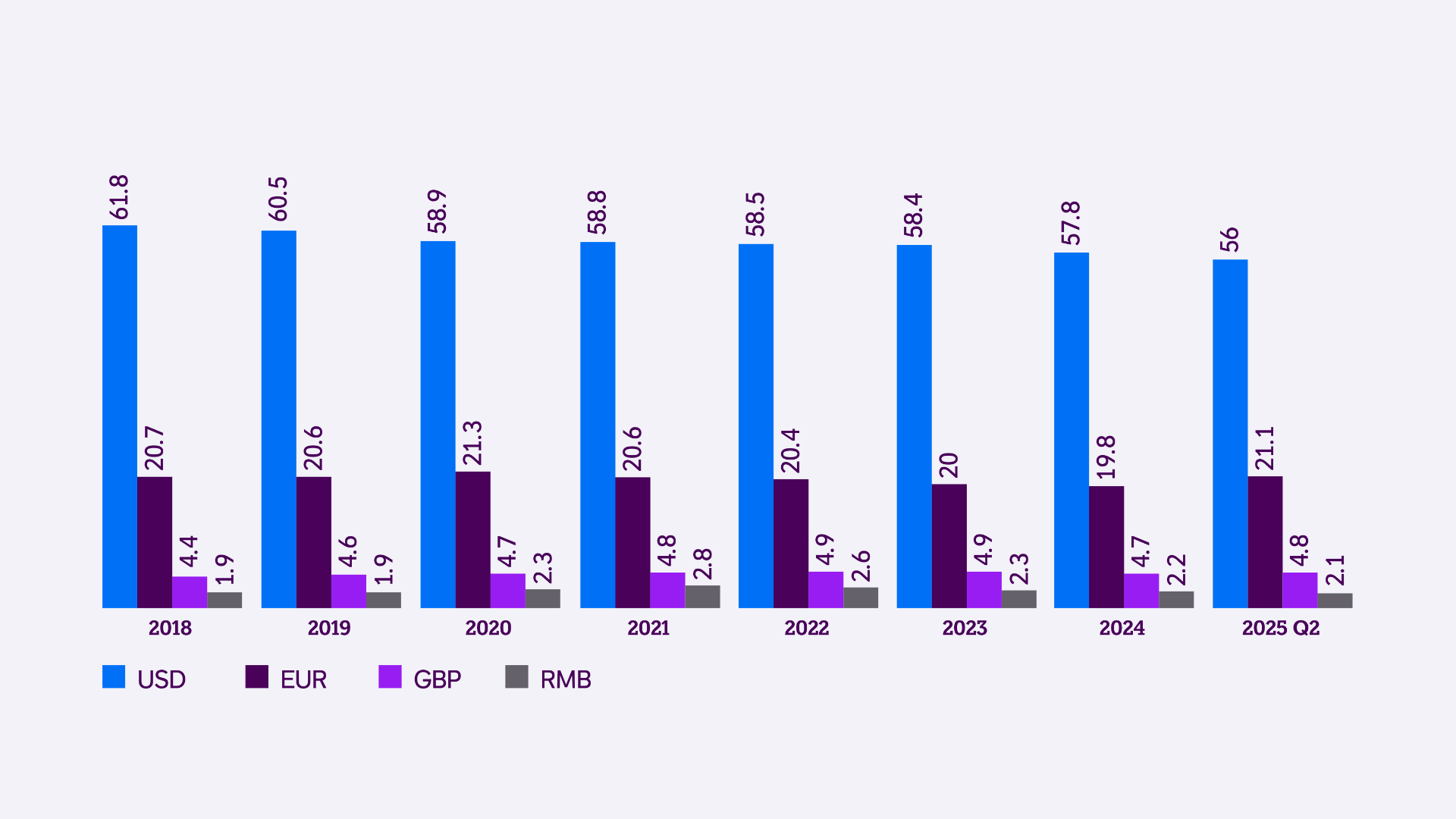

De-dollarisation: from greenbacks to what?

De-day might be a long time coming, yet 2026 could be a year the currency loses more of its lustre.

At a glance:

The world might be seeking an alternate reserve currency, and USD share of reserve holdings has fallen. But there is no clear successor to the dollar.

The Trump administration’s designs on a weaker currency are uncertain.

Hedge ratios of international investors will be key to watch in 2026.

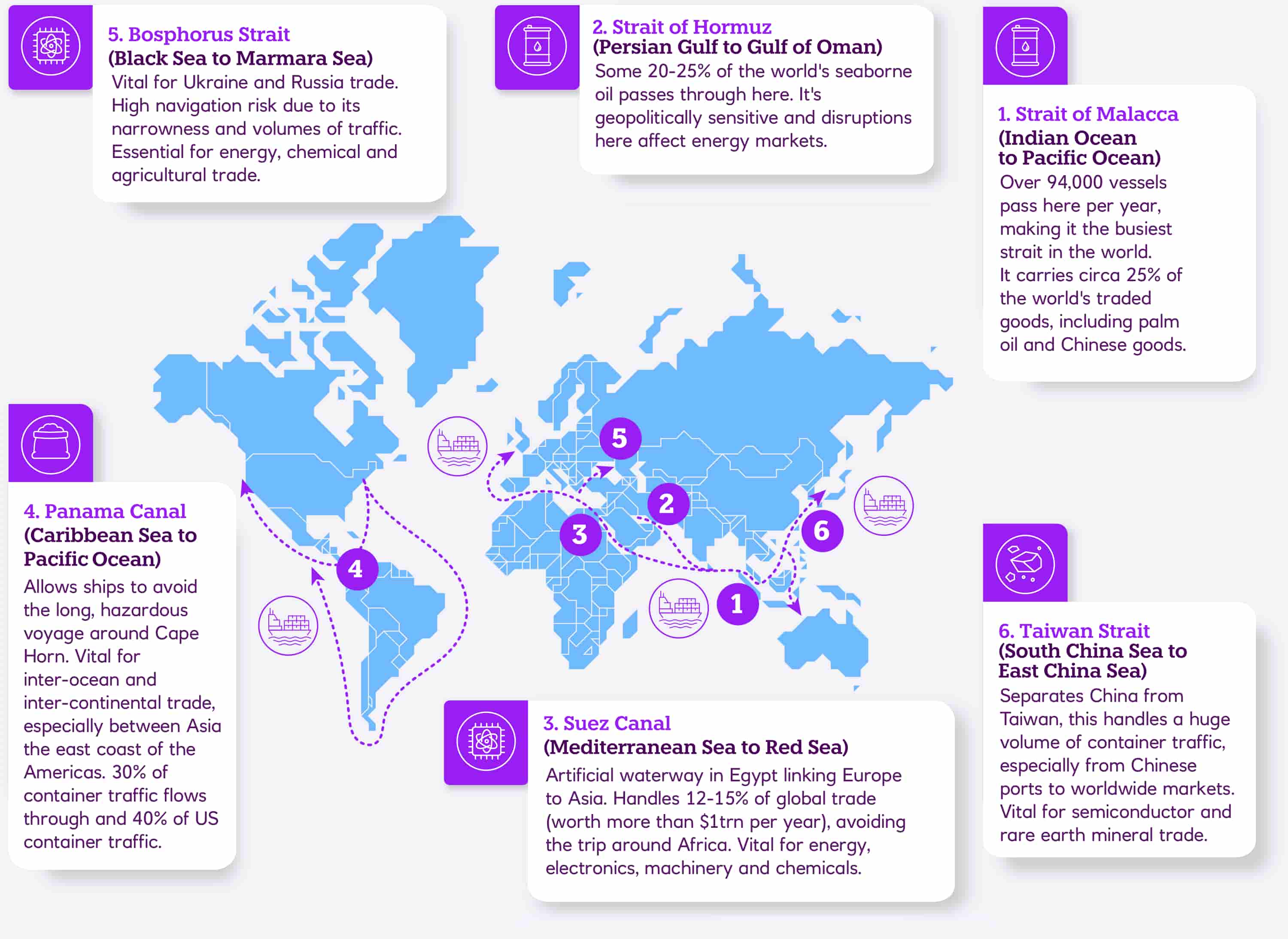

Trade in 26: Rewiring globalisation

As globalisation evolves, economies will feel the combined effects of tariffs, conflict, and possible new alliances over the coming year.

At a glance:

Outlooks for global GDP and trade growth for 2026 are anemic and uncertain, respectively.

Globalisation is evolving, owing to protectionist forces and geopolitics.

Technology and the sustainability transition are developments to watch.

Geopolitics in 2026: a new order for an old world

The outgoing year was marked by conflict and tariff upheaval. But as we enter 2026, will we find new ways to co-operate?

At a glance:

A US-led unipolar order is giving way to a complex multipolar world.

The resilience of modern economies has yet to face a truly systemic test, but 2026 may have one in store.

Nations face returning to hard-nosed realism, without sacrificing stability and co-operation.

Podcasts

Bondcast

Episode 225 - When all is Fed and done

Currency Exchange

Episode 115 - Beyond de-dollarisation

Trade links

Episode 7 - Everything, everywhere, all at once

What will be top of mind for CFOs in 2026?

Guillaume Fleuti, Managing Director, Head of Large Corporates at NatWest, talks uncertainty, opportunity and the pressure to act.

Sustainable finance in 2026: three trends to watch

Improved disclosure, risk quantification and new standards will set the tone for sustainability investments next year. Dr Arthur Krebbers, Sustainable Finance Advisory, NatWest, looks under the hood of the market.

Five predictions for 2026

-

01

Climate resilience goes mainstream.

-

02

Nature finance catches up.

-

03

Sustainable bond issuance remains robust.

-

04

EU Green Bonds gain momentum.

-

05

ESG disclosures enter a transition phase.

Transactions in 2026: Six degrees of integration

For Ritu Sehgal, Head of Transaction Services and Trade, the ways consumers engage with corporates and financial services shape innovation and investment in technology at a time of higher interest rates and macroeconomic change.

Payments in 2026: The magnificent seven

By Lee McNabb, Group Head of Payments Strategy and Digital Assets NatWest

When I consider payments in 2026, I see seven magnificent (and not sinning) influences...

As trade changes, so do our mindsets

Rowan Austin, Head of Trade Origination and Advisory, Corporate and Institutional Banking at NatWest, looks at the trade challenges and opportunities in 2026.

Which innovations will define 2026?

David Grunwald is Director of Innovation and Partnerships at NatWest Group. He explains why 2026 is likely to see renewed focus on artificial intelligence, along with advances in autonomous vehicles, wearable technology and quantum computing.