Markets

The Year Ahead 2022: What a 'World of Shortages' means for markets, companies, and the economy

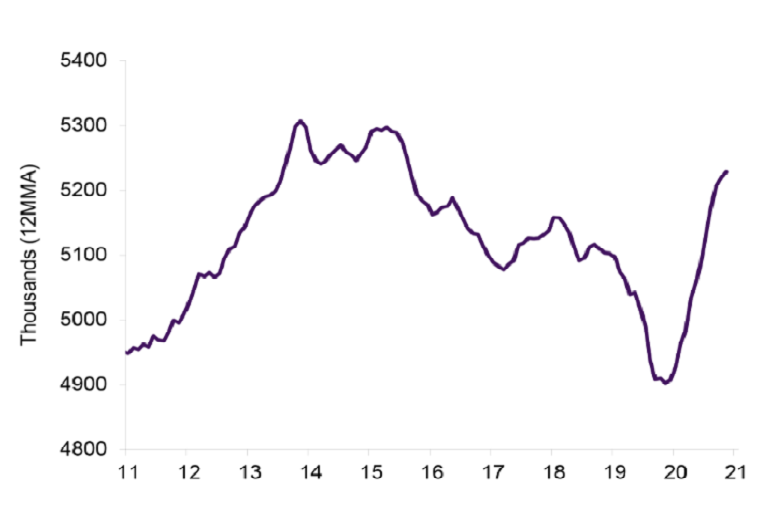

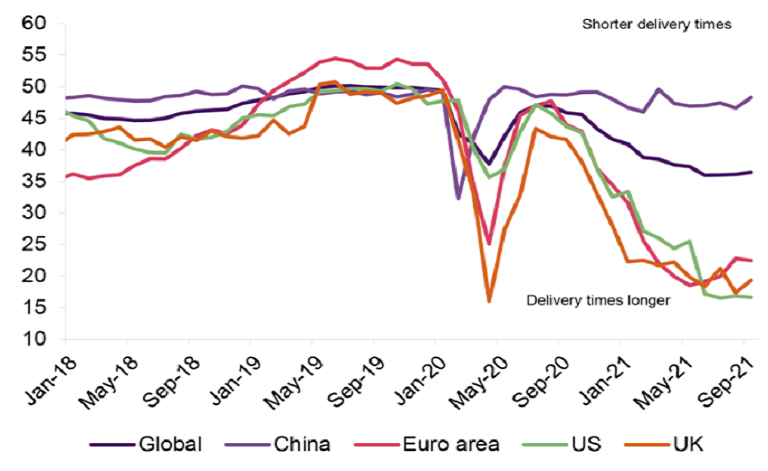

As the global economy has reopened, demand has clearly outpaced the supply of nearly everything from skills and labour to energy and commodities, and big questions remain over the scale and persistence of the disruption in the year ahead.

22 Nov 2021

. 4 min read

We take a closer look at how long they’re likely to last and the major implications for key sectors, markets, and regions.