Markets

The Year Ahead 2022: Six ways China’s ‘Common Prosperity’ policy could affect the global economy

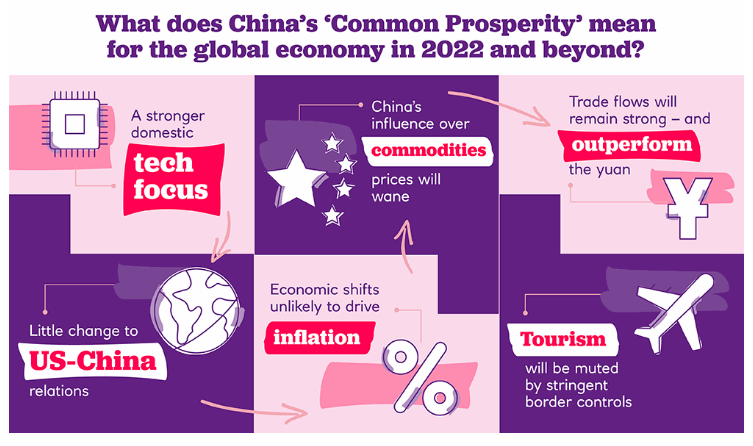

China’s “Common Prosperity” policy looks set to be a game changer for the country as it refocuses its priorities away from economic expansion at breakneck speed at any cost towards a long-term goal of reducing domestic inequality in the years to come.

22 Nov 2021

. 4 min read

We consider some of the key implications of the new policy and what they mean for the global economy.