Markets

The Year Ahead 2022: From Big Fiscal to Big Consumer – and how central banks will react to the transition

We take a closer look at the handoff from generous fiscal policy to consumption-led growth in the year ahead, how central banks could react to new inflationary pressures, and what all of this means for markets.

22 Nov 2021

. 4 min read

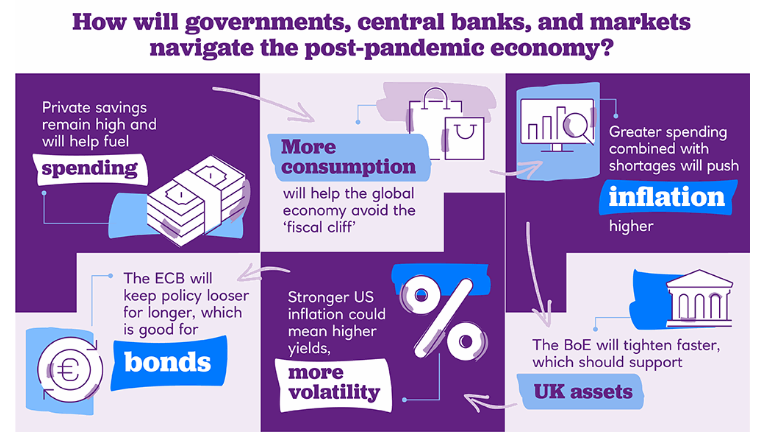

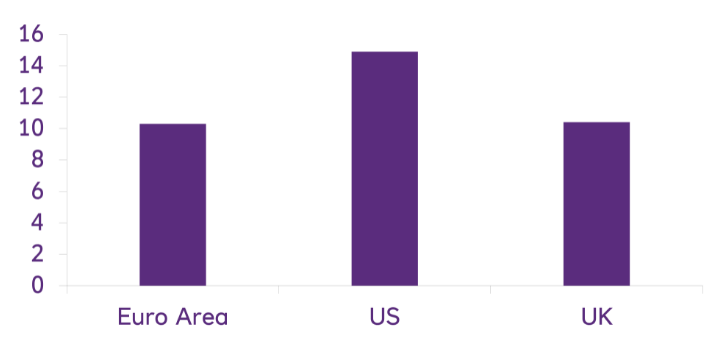

Private savings skyrocketed in all major advanced economies during the pandemic, with government furlough schemes filling people’s pockets at a time when lockdowns curbed opportunities to spend.