Markets

The first 100 days of Brexit: the search for a new economic paradigm continues

The first 100 days of life outside the EU already provide a glimpse of the practical challenges facing UK corporates & investors, and raise one all-important question: what is the UK’s longer-term economic vision? Ross Walker provides his quick take here.

29 Apr 2021

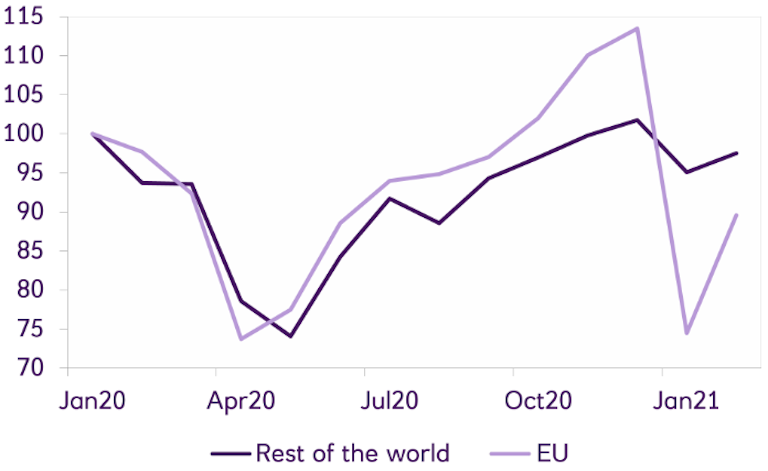

Brexit has been described as a process, not an event, and economically, the process remains embryonic, with limited hard data to make a clear assessment. Still, although some of the most visible disruption – motorways in the south east of England becoming lorry parks – has been avoided, trade data hints at challenges ahead.