Markets

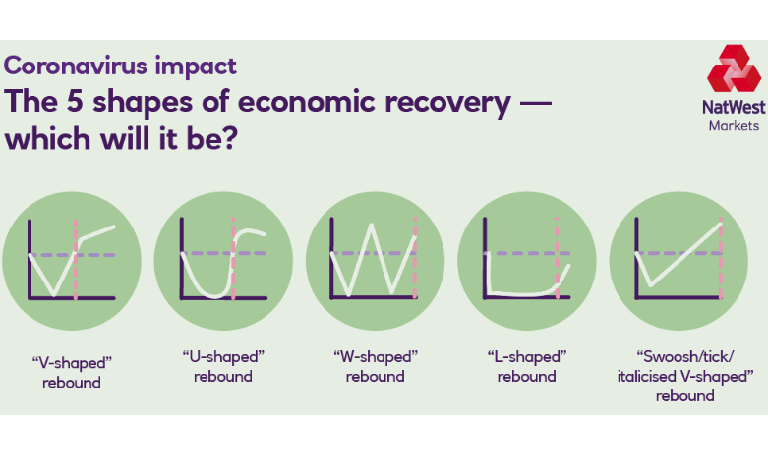

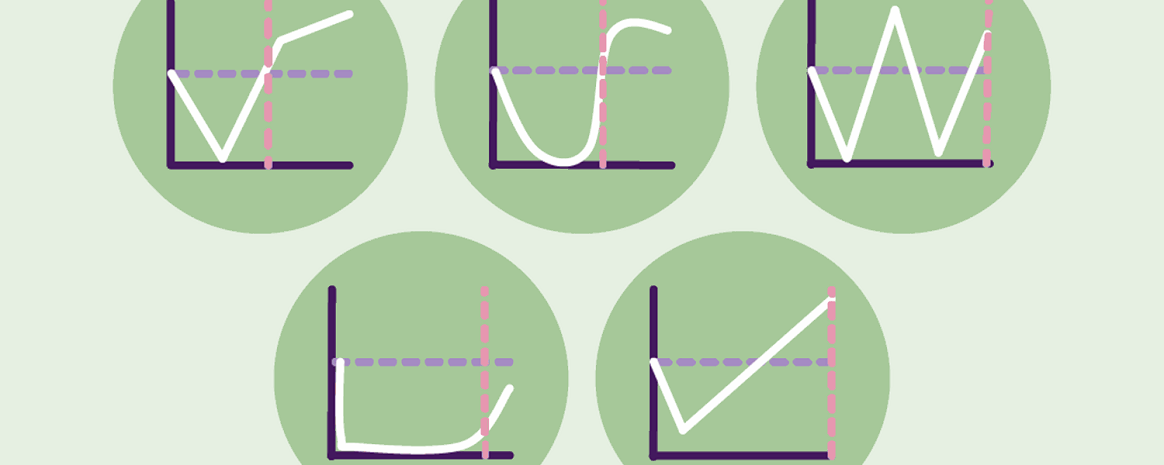

The 5 shapes of coronavirus economic recovery and why our base case is a “swoosh”

There has been lots of talk about what the shape of economic recovery might be. We expect a “swoosh-shape”. Here’s why.

22 Apr 2020

. 5 min read

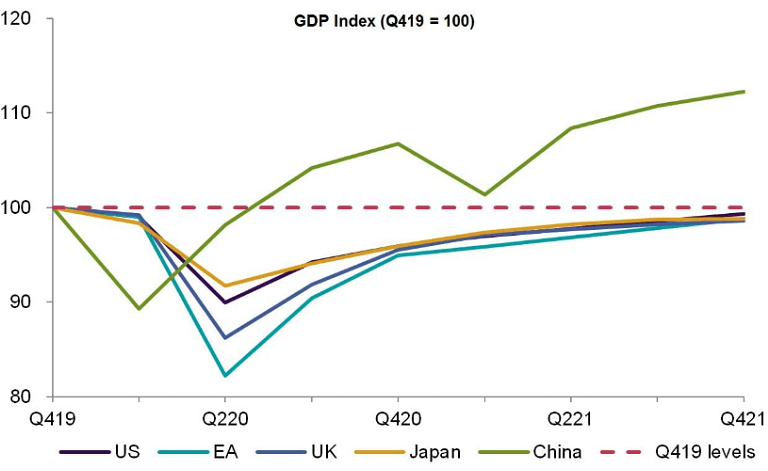

Our current forecast calls for a staggering 10% decline (peak-to-trough) in global growth (GDP) in the first half of 2020.