Markets

The 2021 outlook revisited: which key calls could come to life in Q2?

Our Global Head of Desk Strategy John Briggs reflects on how some of the major calls from our Year Ahead 2021 outlook are evolving – and their impact on economies & markets in the months to come.

08 Apr 2021

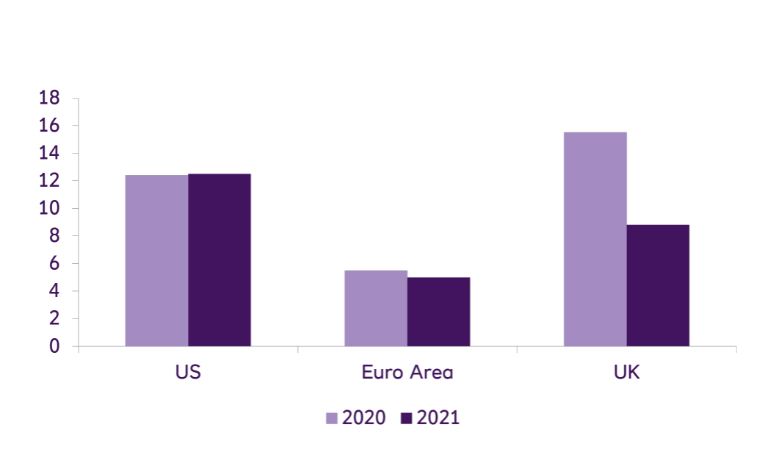

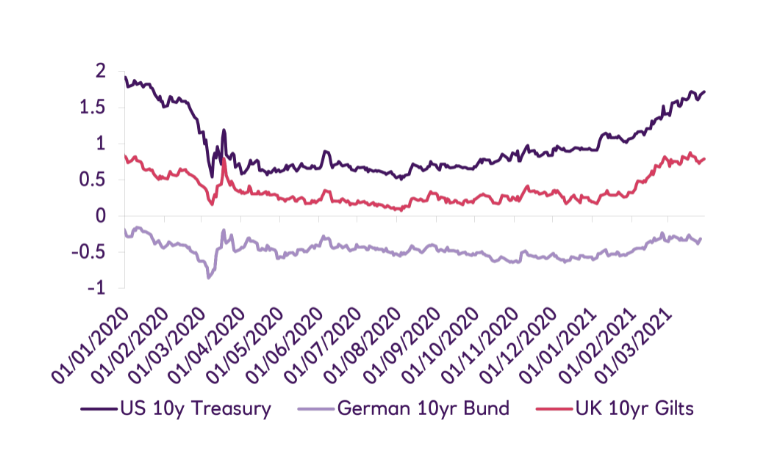

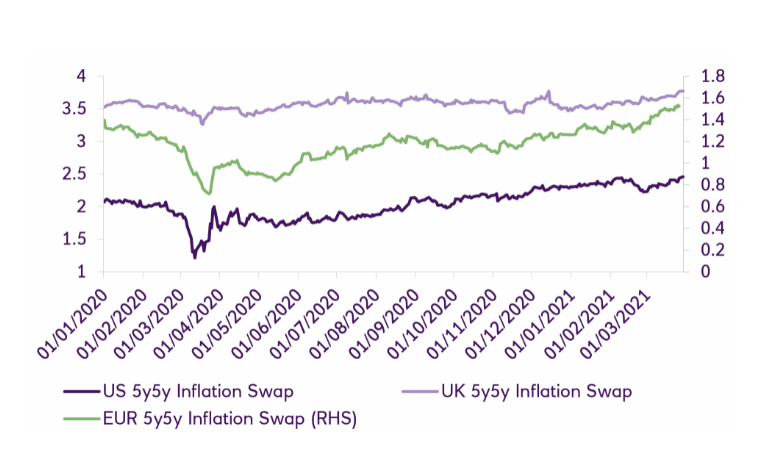

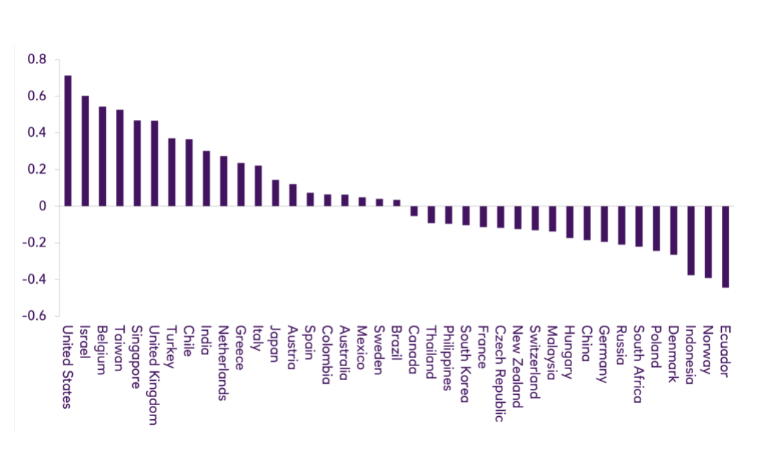

The first quarter of 2021 has been eventful to say the least: from the realities of Brexit setting in, a new US administration, lockdown woes exacerbated by varying degrees of global vaccine hiccups, a reflation rout in bonds and myriad central bank responses, to idiosyncratic volatility in emerging markets (EM), discussion of a new commodity super cycle, a strong rally in cryptocurrencies and the rise of the “meme” stocks.