Shortages of skilled labour create significant risk. In manufacturing, construction, health and social care, and in parts of hospitality, the third lockdown has led to labour shortages. This may prove a medium to longer term problem, according to businesses we’ve spoken with, rather than a short-term issue. Whilst the increase in unemployment has not been as significant as feared, the drop in labour force participation, albeit only 1%, is feared to reflect a more permanent change in the domestic labour supply.

The years that followed the global financial crisis (GFC) may be particularly instructive on the risk posed by rising commodity prices. The global economy has become fairly accustomed to cost push-inflation (when overall prices increase due to higher input costs) since the global financial crisis of 2008-09, when a significant bout was observed. Having hit multi-year lows in 2009, the CRB index, which reflects the price of a broad basket of commodities, rose over 75% in the space of under 2.5 years. That rise in commodity prices was in part speculative, rather than due to shortages. So signs of commodity price inflation seen more recently – the doubling in commodity prices since March 2020, according to the CRB index – are not wholly unexpected. In this case though it may in part be supply side driven, rather than purely due to demand side ‘speculative’ activity.

Freight costs are rising, making supply chains more expensive. The Baltic Exchange Dry Index rose from just over 1350 at the end of December 2020 to a peak of 3266 in early May 2021.Why? The past six to nine months have seen a growing shortage of shipping containers in Asia, used to ship goods to the West. With limited transit of goods from Europe to Asia, the UK and Europe have accumulated a surplus of containers – making shipping from the Far East more difficult and expensive. The short-term solution has been to incorporate the cost of shipping the empty containers back to their port of origin into the cost of shipping goods. This may become a longer-term solution unless more goods are shipped from the UK and Europe back to Asia.

Additional pandemic-related costs need to be navigated. Businesses that have been forced to close during lockdown for long periods have taken on additional costs. The costs associated with becoming more coronavirus-secure, taking on extra debt to stay afloat, delaying rent and rates payments, as well as reduced capacity limits lowering business income are all likely to lead to higher prices (and already has in some areas of services).

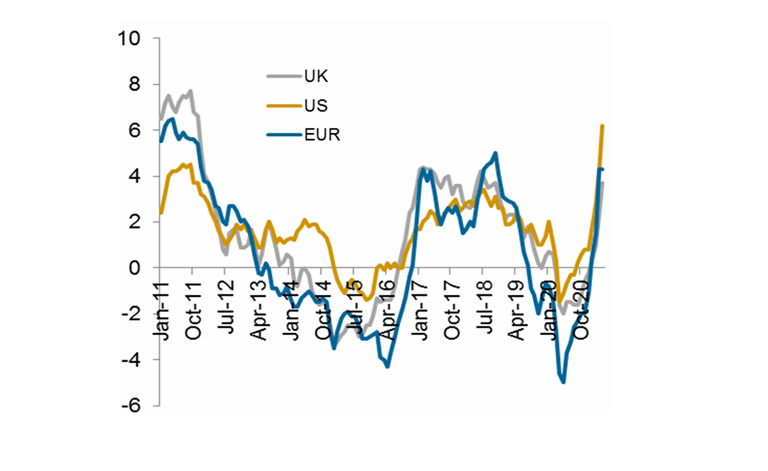

Supply chain disruption is becoming more commonplace in the wake of Brexit and the pandemic. Businesses in construction, manufacturing and wholesale have repeatedly mentioned supply shortages, with a variety of materials and semi manufactured goods seeing demand outpace supply. This is evident in the pace of producer output price inflation, although this has, so far, accelerated more quickly in the US and the Euro Area than the UK.

In construction and some parts of manufacturing, material prices have risen sharply as a result of shortages and some speculative price hikes (to take advantage of the supply/demand imbalance). We can see how producer price inflation has spiked in the chart below. It’s important to note that it’s not the level of producer price inflation that’s the issue – it’s the speed of the swing from deflation to inflation, which has been far faster than anything we’ve seen over the past decade. Nevertheless, in conversation with businesses in these sectors, those that face materially higher input costs note that their clients seem to be less resistant to the prospect of raising their prices than expected.