Markets

Global economic forecast for 2021: continuing global divergence

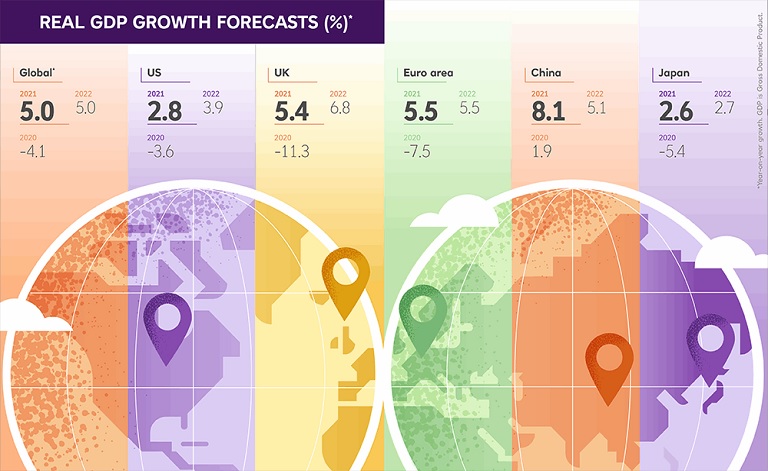

Following a year when lockdown measures caused a global recession, how will the recovery shape up in 2021? We’re cautiously optimistic about the year ahead but divergence will remain a defining theme in 2021.

03 Dec 2020

While 2020 brought an unprecedented economic shock, 2021 will bring vaccines and a marked turnaround in economic performance – though that performance is unlikely to be even.