Markets

Decade ahead: 7 unthinkable (but not impossible) forecasts

If the coronavirus crisis taught us only one thing, it would be that the future of the world can turn on a dime and anything is possible.

22 Jun 2020

So, we asked five of our specialists to use their wildest imagination in an outlook for the decade ahead. Is it totally wacky, or actually plausible?

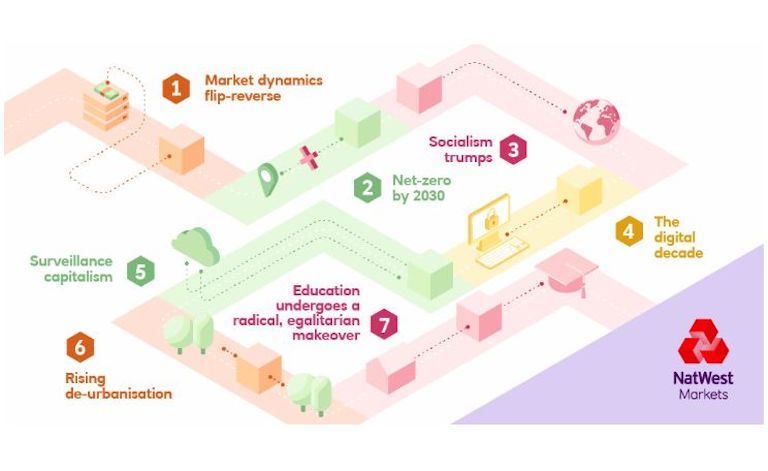

Socialism trumps

Nationalism takes over the west, Asia soars to the top, Europe divorces and globalisation declines.

In his Q&A, Phil asks if it is totally wacky to question whether rising populism in western society over the last decade might have paved the way for a full socialist agenda. Social priorities such as healthcare and welfare benefits have risen to the top of the agenda during the coronavirus crisis.

Meanwhile Jim thinks the gravitational pull of economic power towards Asia could become irresistible. Could the Chinese renminbi become the world’s reserve currency and overtake the US dollar? In his view, the strength of Asia is a force that isn’t going away — especially China. But Jim explains they are the new kid on the block and it will take them a while to shake that image and to build trust.

Jim also debates whether the coronavirus crisis is going to help answer if the European countries can stick together. Both outcomes would be a pretty big event and if Europe does actually divorce, it could lead to another crisis.