Markets

China’s dual-track economic recovery in 2021: should markets be worried about tightening financial conditions?

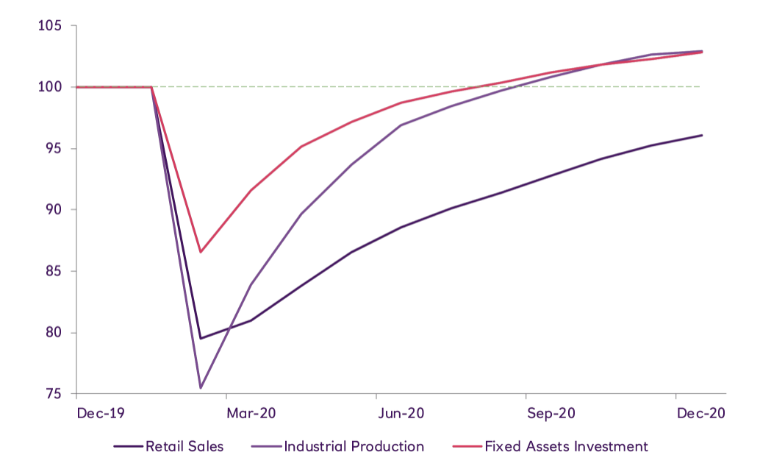

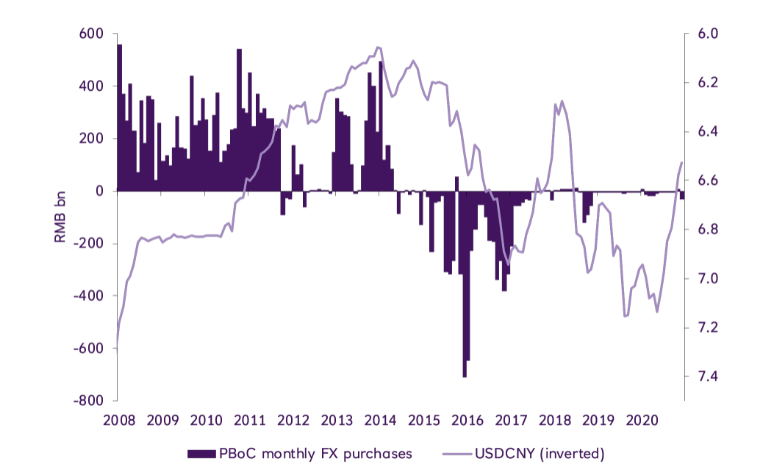

With a dual-track economic recovery taking shape in China, markets have grown increasingly wary of tightening financial conditions. Is there cause for concern?

02 Mar 2021

. 4 min read

In this quick-take article, our China Economist Peiqian Liu explores three key reasons why tightening fears are overblown.