Finances

Trade V-Covery: will supply chain bottlenecks scupper a trade recovery?

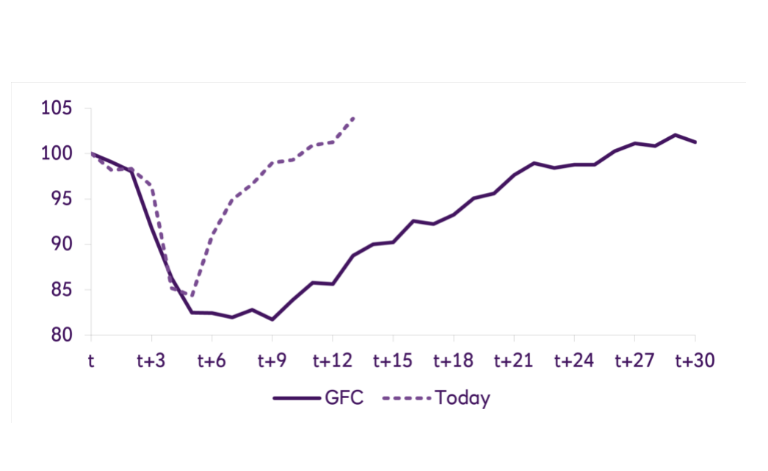

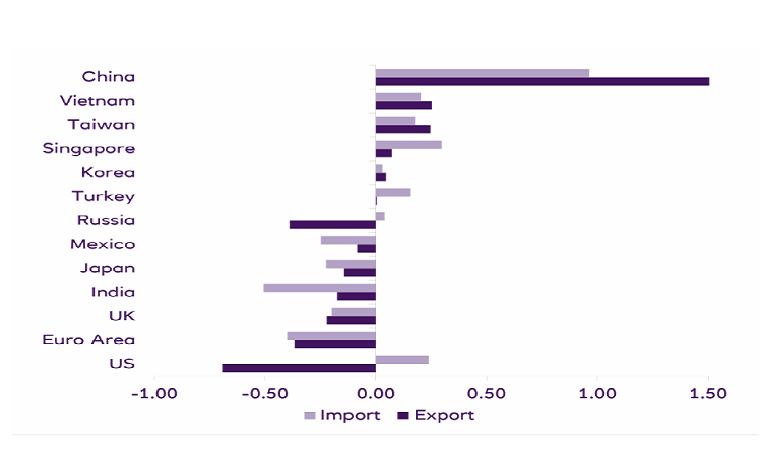

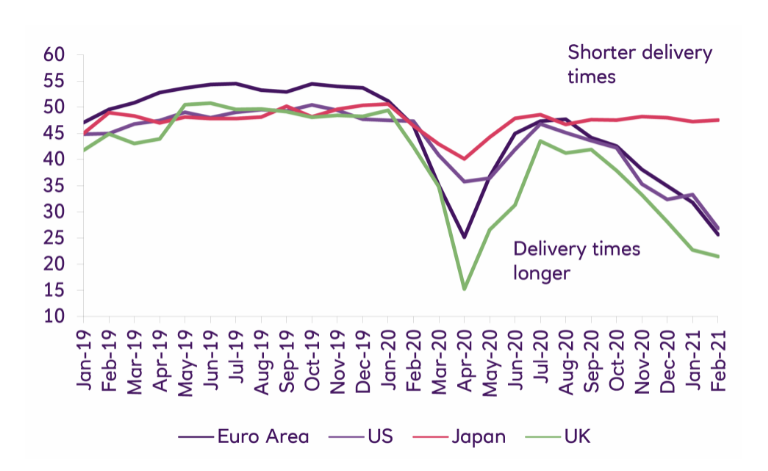

Global trade continued its impressive recovery in the early months of 2021 but risks still weigh on the outlook as many countries continue to reopen.

22 Apr 2021

. 4 min read

Our specialists outline several key reasons why the shape of the global trade recovery may change as we move through the second quarter – and what corporates can do to mitigate supply chain risk.