Finances

Tracking trade: when will supply chain and price pressures ease?

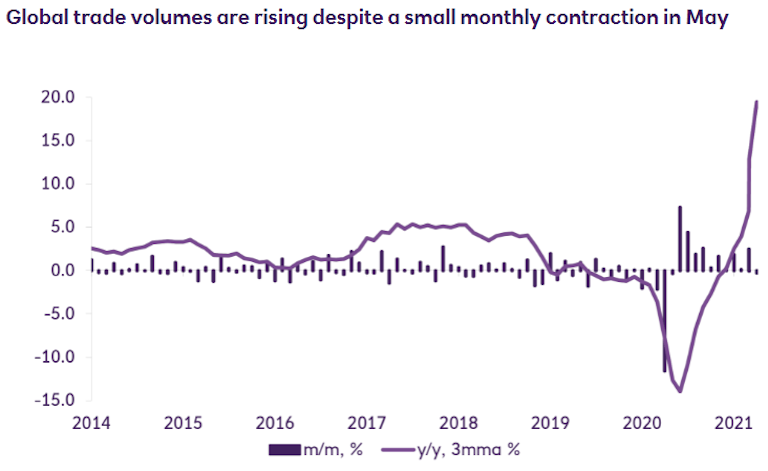

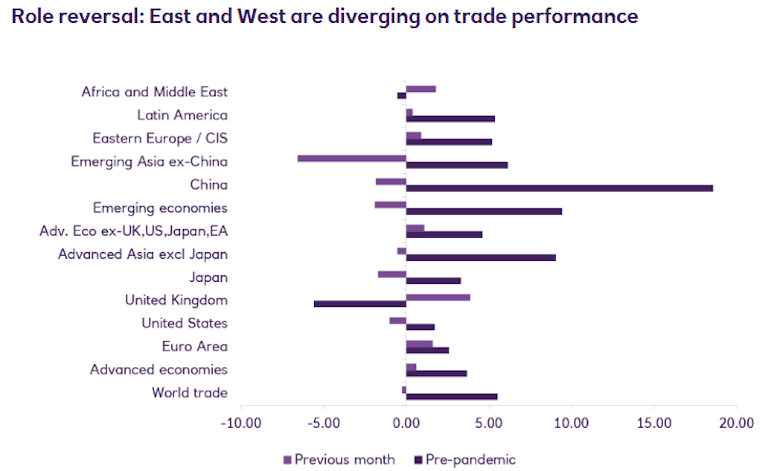

While trade ramps up in the UK and Europe, Asian economies continue to see a slowdown.

16 Aug 2021

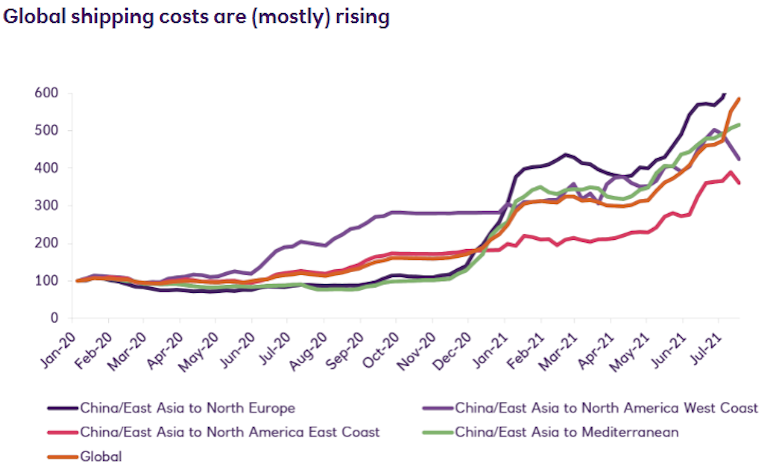

The divergence between East and West puts additional pressure on supply chains and prices and raises yet more concerns about the effect of inflation on corporates in the second half of 2021. In this quick-take, Economist Peiqian Liu takes a closer look at some of the latest trade trends and explains why transportation costs, margin and supply pressure should recede as reopenings continue.