Conglomeration – the process by which a company acquires businesses with the intention to diversify or become a ‘conglomerate’ – was all the rage back in the 1960s and 70s. Firms sought to expand through mergers & acquisitions (M&A), backed by research that suggested diversifying their businesses should reduce their overall risk profile during difficult periods, achieve better economies of scale, attract more capital and become more efficient in deploying it through internal capital markets.

But the tide began to turn from the 1980s onwards, as research pointed to numerous disadvantages of a conglomerate model. These included information asymmetries between central managers and divisional managers, the high costs of moving in and out of businesses (compared with investors’ ability to do so), and the agency problem which could lead to managerial empire-building. Most infamously, one study estimated that, on average, a conglomerate’s firm value can be 13-15% less than the sum of its parts, implying a significant ‘conglomerate discount’ as a result of diversification[1]. This marked the rise of the deconglomeration trend.

Differing effects from different perspectives

Any company mulling a de-merger needs to consider the effects on value from different stakeholders’ perspectives, including equity and debt investors.

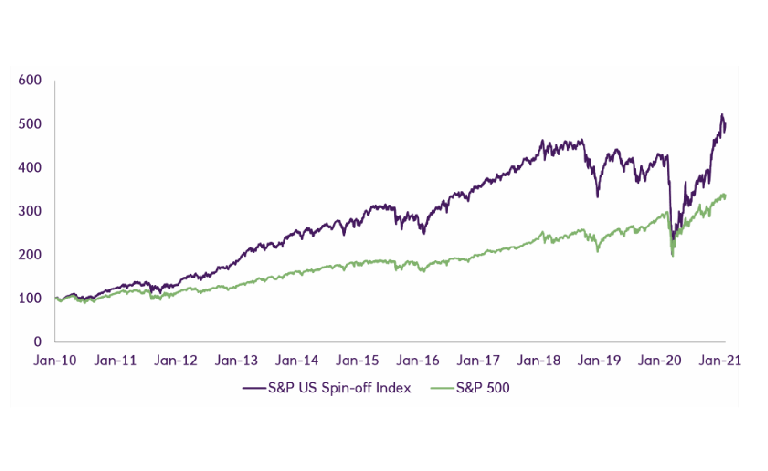

Equity markets and shareholders are typically supportive of de-merger activity. S&P Capital IQ’s Quantamental research looking at corporate spin-offs and carve-outs between 1989-2015 shows spun-off entities generated long-term outperformance against the broader market[2]. This is further evidenced in the graph below, where the S&P US spin-off index[3] has shown to outperform the wider S&P 500 index by more than 50% in the last 10 years.

However, credit stakeholders can be less sympathetic. This is mainly because scale and diversification are typically seen as credit-positives, and a de-merger could be considered as a potential trade-off between a weaker business risk profile (smaller scale, less diversified) for a potentially stronger financial risk profile (through the use of proceeds in deleveraging). As a result, a corporate implementing a de-merger needs to carefully consider potential credit implications during its stakeholder management process.

Stocks of spun-off companies have outperformed the broader market in the past 10 years