Finances

Corporate funding and the economic recovery: why UK businesses should be optimistic about the months ahead

In this quick-take article, Ross Walker dives into the latest UK corporate funding & sentiment data and highlights several key reasons why businesses should be optimistic about normalising conditions as the country slowly – but surely – escapes the pandemic’s grip.

20 Apr 2021

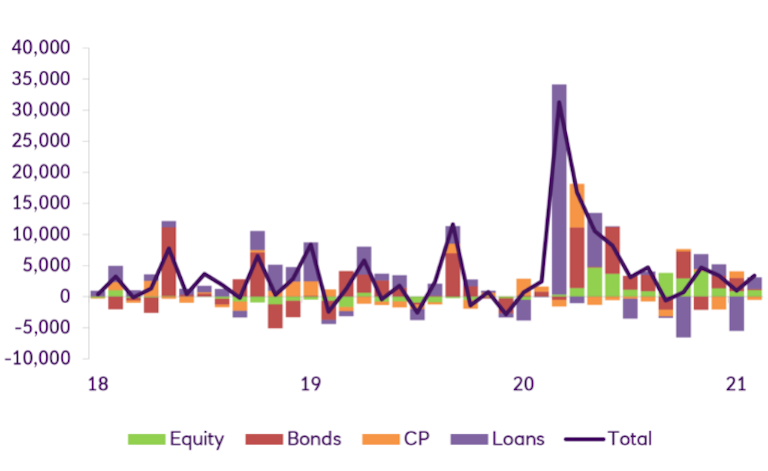

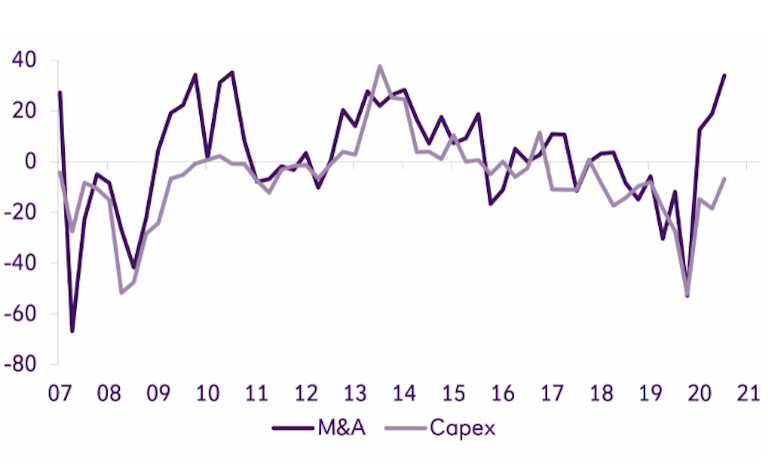

With the UK’s reopening slow but sure, yet more signs of economic normalisation are starting to emerge.