US: will investments continue?

Reflecting the impact of the Inflation Reduction Act (IRA), new investment in clean energy technology over the past 12 months was up 165% compared with five years ago, and stands at more than $200bn according to the Clean Investment Monitor. But could some of the initiatives be at risk if the political backdrop changes over the next few years?

We believe 2024’s elections are unlikely to represent a challenge to the green investments currently under way. Many have been made in Republican-leaning states and the focus on subsidies in the IRA has made the theme appealing across the political spectrum. Pushing against investment incentives in the 2024 election campaign might not be a vote winner.

The future of many of these initiatives is more dependent on bureaucratic processes than ideology or the political balance of power, such as bottlenecks in gaining permits for clean power projects.

EU: do voters want faster decarbonisation?

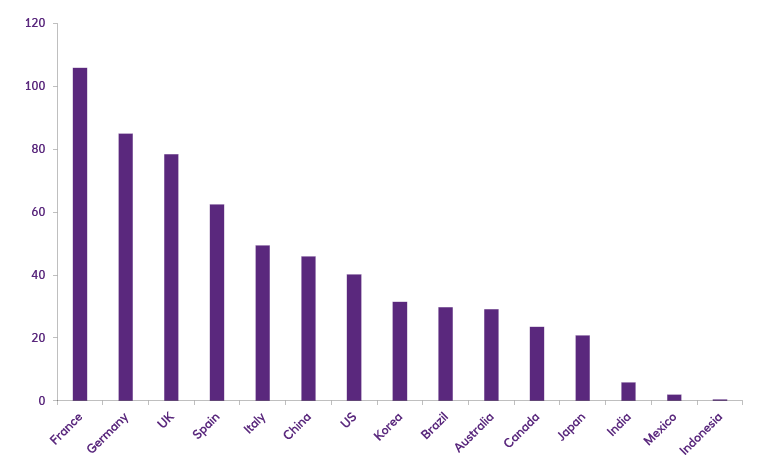

According to the IEA, the European Union (EU) has made steady progress towards its goal of cutting greenhouse gas emissions by 55% from 1990 levels by 2030, in line with the 2019 European Green Deal. A record 41GW of photovoltaic capacity and 16GW of wind capacity were installed in 2022, as Europe sought to reduce its dependence on fossil fuels from Russia. Renewables now supply 39% of the EU’s electricity, says the IEA.

Europe’s Green Industrial Plan is designed to reduce dependence on imports of net zero technologies, diversify supply chains and scale up the domestic manufacturing capacity to support the transition. But it remains to be seen how high energy prices, concerns about energy security and extreme weather events affect voter sentiment towards faster decarbonisation.

Coal still a problem in China

As the world’s highest emitter, China’s ambition to reach peak emissions by 2030 and carbon neutrality by 2060 are critical for the global transition’s success. And it has been vigorously developing green and low-carbon industries such as electric vehicles, solar photovoltaics, and offshore wind power; indeed, it now commands a status as one of the world’s leading producers across all three.

But China’s consumption of coal remains a major problem as it still accounts for nearly 70% of the country’s total emissions. China’s authorities haven’t yet committed to a specific target for reducing emissions from coal, probably due to its role in ensuring security of supply. So, while China has set ambitious targets and is promoting cleaner technologies, it has more work to do.

Can India catch up?

India's biggest challenge is to balance its development needs with environmental sustainability. Significant investment and international co-operation will be needed to achieve its net zero target by 2070. It’s made some progress: figures from the IEA say its renewable energy accounts for more than 40% of its energy capacity. What’s more, the government has announced a slew of measures to promote renewable energy, green hydrogen, energy storage and electric vehicles.

The most glaring issue is that India still lacks a strategy to phase out coal. Under its latest electricity plan it intends to build substantial new coal power capacity between 2027 and 2032. This reasonably raises questions about its ability to meet its net zero targets.